What is the Canada Pension Plan and how does it work?

The Canada Pension Plan (CPP) is a mandatory public pension program designed to provide partial income replacement in retirement. With fewer employers offering defined-benefit pensions and more Canadians relying on self-directed savings, the Canada Pension Plan has taken on an even more vital role. Its broad base, steady funding, and professional management ensure that even workers without substantial private savings have a solid foundation for retirement.

Introduced in 1966, it was created at a time when Canadians were living longer and traditional employer pensions were less reliable or widespread. Today, nearly every worker in Canada outside Quebec (which runs its own Quebec Pension Plan, or QPP) contributes to CPP. It’s one of three pillars of Canada's retirement income system, alongside Old Age Security (OAS) and private savings such as the Registered Retirement Savings Plan and workplace pensions.

The three pillars of Canada’s retirement income system

How the Canada Pension Plan works

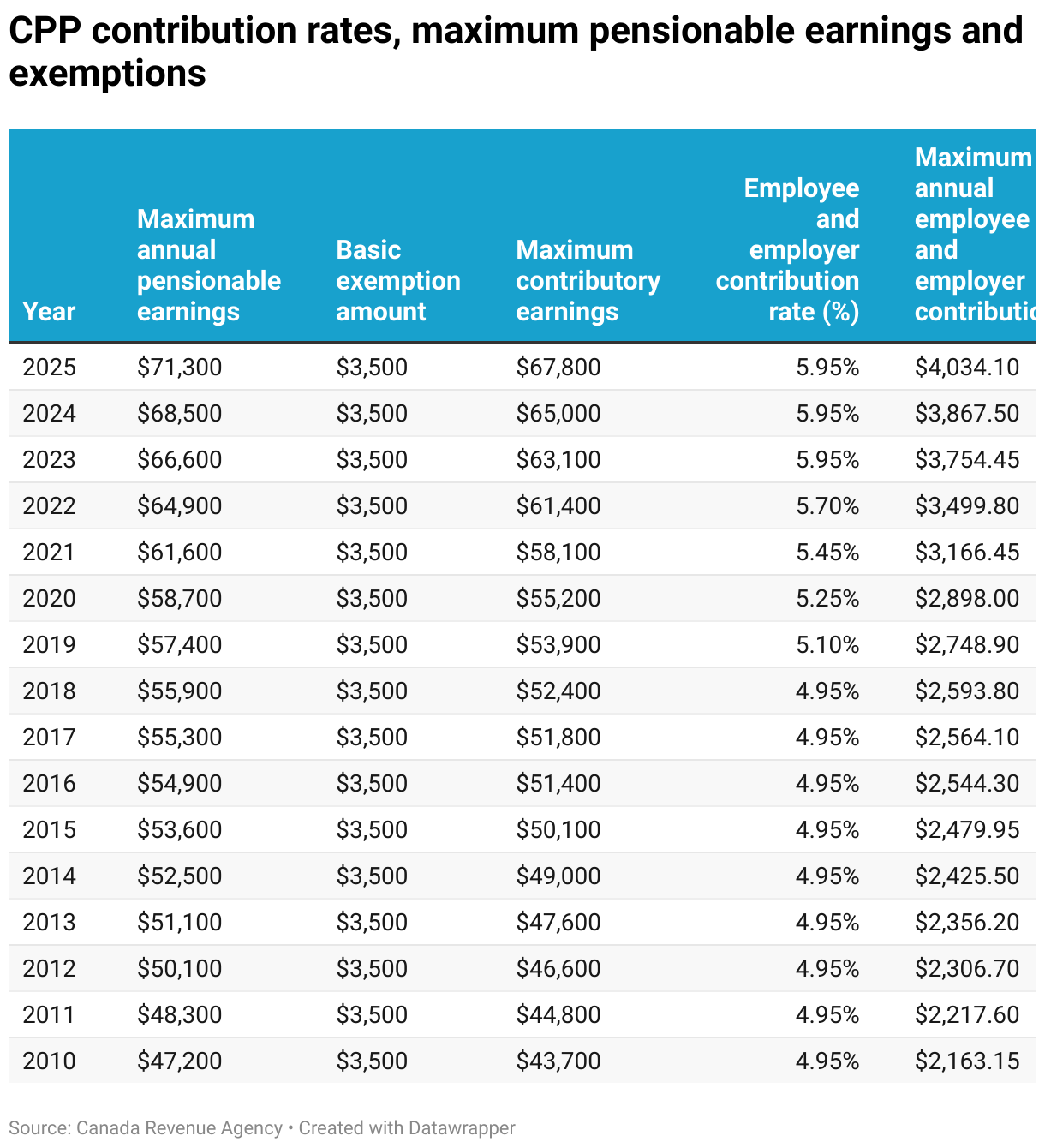

The CPP is funded through contributions from both employees and employers. In 2025, the contribution rate is 5.95% of pensionable earnings for each—meaning a combined 11.9%. Self-employed individuals pay both shares.

Crucially, the CPP is not a traditional government-funded pension paid from tax revenues like Old Age Security. Rather, it is a contributory, earnings-related, and portable plan. That means the benefits you receive are directly tied to what you—and your employer—have paid into it. In 2025, contributions apply to earnings between $3,500 and $71,300.

What benefits do Canadians receive from CPP?

CPP provides a monthly payment to retirees, but that’s not all. The program also offers:

Disability benefits for those who become severely disabled and can no longer work.

Survivor benefits for spouses or common-law partners of deceased contributors.

Children’s benefits for dependents of disabled or deceased contributors.

Death benefits—a one-time payment to help cover funeral costs.

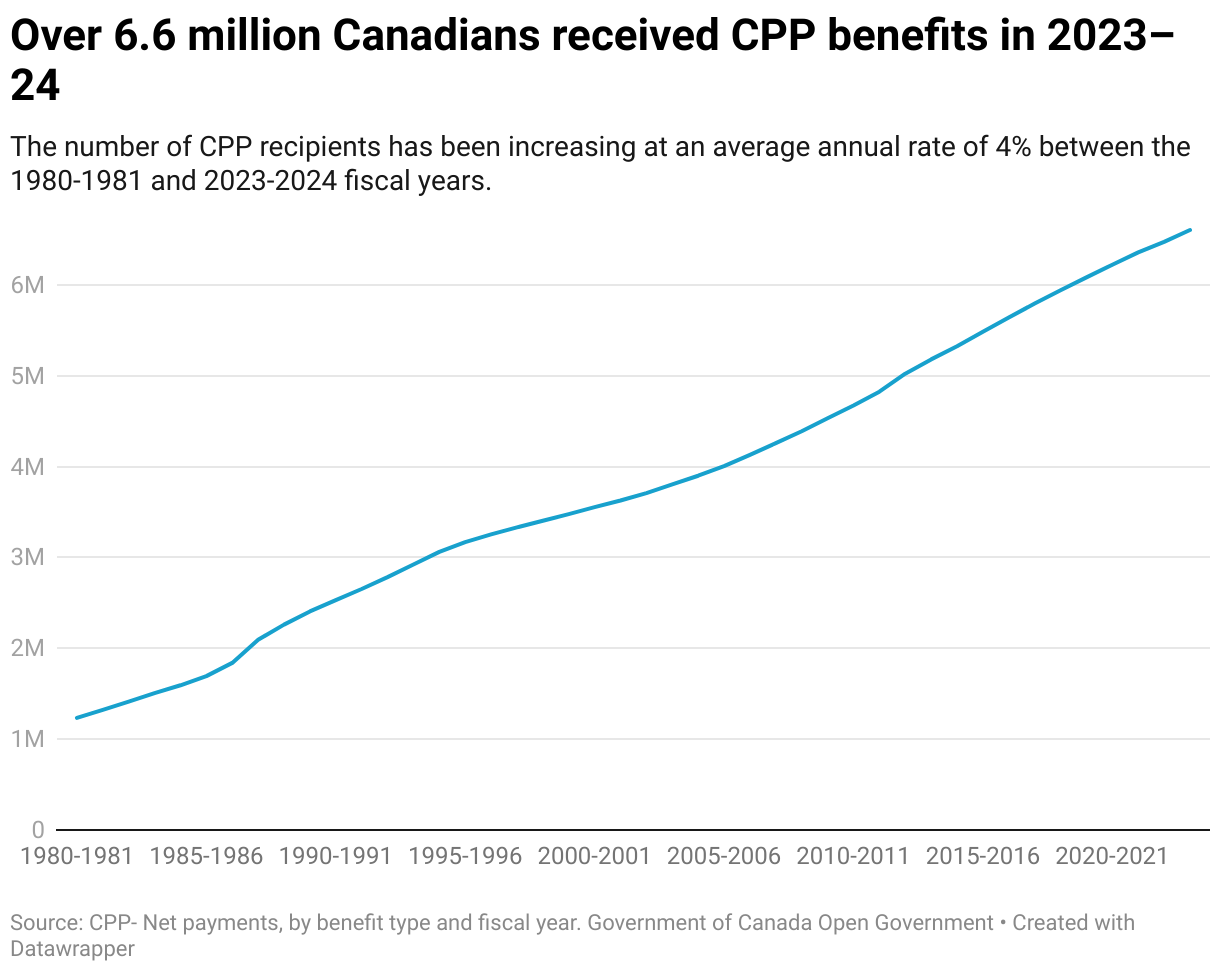

There are about 22 million CPP beneficiaries and contributors, underscoring the important role the Fund plays in providing Canadians with a solid foundation in their retirement years. In the 2023-2024 fiscal year, approximately 6.6 million Canadians received CPP benefits, with total payouts reaching over $60 billion. Of which, $48 billion was paid to retirees; $4.5 billion went to disability benefits; $5.3 billion was paid out in the form of survivor benefits, $492 million was in the form of death benefits; and $565 million was paid out to dependents of disabled or deceased contributors.

The number of CPP recipients has been increasing at an average annual rate of 4% between the 1980-1981 and 2023-2024 fiscal years. Meanwhile, total CPP benefits paid out have increased by about 8% annually during the same period.

The CPP has several progressive features to help individuals and families. One of the key features of the Canada Pension Plan is indexation. The CPP is designed to keep up with changes in the cost of living, and payments are adjusted in January of each year to reflect increases in the Consumer Price Index published by Statistics Canada. For families, one key feature is pension sharing. This allows spouses or common-law partners who are together and collecting CPP benefits to share a portion of their pension partner even if only one of them has contributed to the plan. While this doesn’t change the amount received, it can result in tax savings.

As of October 2024, the average monthly CPP retirement benefit for beneficiaries was $899.67, or $10,796.04 per annum. The maximum amount that could be received at age 65 was $1,433.00, or $17,196 per annum, based on January 2025 figures. The actual amount depends on how much and how long you've contributed, and at what age you begin to collect (you can start as early as 60 or as late as 70).

Who manages the CPP funds?

The responsibility of managing the Canada Pension Plan’s funds falls to the Canada Pension Plan Investment Board (CPPIB), a Crown corporation established in 1997 that operates independently of the CPP and the federal government. The CPPIB’s objective is “to maximize long-term investment returns without undue risk, taking into account the factors that may affect the funding of the Canada Pension Plan and its ability to meet its financial obligations.”

The CPPIB invests in a globally diversified portfolio across public equities, private equity, real estate, infrastructure, and fixed income assets. Holdings span more than 50 countries and include logistics hubs, renewable energy, and major tech companies. The CPPIB has demonstrated a strong track record of being a prudent steward of the CPP’s funds. At the end of its fiscal year ending on March 31, 2025, the CPPIB reported having more than $714 billion in assets. That fiscal year, it recorded $59.8 billion in net income, one of the highest on record. The strong returns are in line with the Fund’s performance over the past decade. As of March 2025, its 10-year annualized net return was 8.3%. This prudent stewardship is a major reason why the CPP is projected to be sustainable for at least the next 75 years.

While CPP alone won’t fund a luxurious retirement, it’s designed to be there—steady and predictable—when Canadian retirees need it most. Sound management of the funds by CPPIB will help ensure Canadians have firm financial support during their retirement years.